Three years ago, Cinven, a British private equity firm, was actively pursuing the acquisition of segments within Europe’s relatively stagnant life insurance industry.

At the time, Cinven’s portfolio included medium-sized life insurance companies in Italy and Germany, which it had significantly expanded during a period of low interest rates. This expansion involved acquiring annuity portfolios from other insurers.

A newly established €1.5bn fund, the firm’s first dedicated to financial services companies, aimed to leverage Cinven’s established success in investing within the sector. Caspar Berendsen, a senior dealmaker at Cinven, emphasized the group’s strong track record in this area while leading the strategic initiatives.

Initially, Cinven projected positive returns from its investment in Eurovita in Italy, and it displayed notable confidence in its German life insurance asset, Viridium. The firm even restructured its ownership of Viridium between funds to prolong its control and advance its consolidation agenda.

However, the situation took a downturn subsequently. Eurovita faced insolvency the following year due to a surge in interest rates that revealed vulnerabilities in its financial structure. Cinven opted not to inject the additional capital requested by regulators, leading to a mass exodus of the insurer’s policyholders.

Following these setbacks, Berendsen departed from the firm and refrained from providing any comments on the matter.

Moreover, Viridium’s ambitious deal to acquire a $20bn back-book from Zurich encountered obstacles. Reports suggest that Germany’s financial regulator was inclined to block the transaction due to concerns stemming from the Eurovita incident and uncertainties surrounding the private equity fund’s ownership model.

This series of events has cast doubt on the viability of the private equity-backed consolidation strategy in the life insurance sector. According to sources familiar with Viridium’s perspective, sustaining growth hinges on establishing an ownership structure that aligns with regulatory requirements.

While Cinven chose not to offer a formal statement, insiders familiar with the firm’s stance highlighted its substantial financial contributions to Eurovita, including repurchasing bonds during the liquidation process. They also emphasized Viridium’s robust financial position.

These developments have posed a significant challenge to private capital groups venturing into the life insurance domain. The Eurovita episode, in particular, has been viewed as a setback in the relationship between private equity entities and regulators, eroding years of collaborative efforts.

Moving forward, there is a growing call for heightened scrutiny of the unique risks associated with insurers and their policyholders amidst the increasing influence of private equity in the sector. Regulatory bodies, including the IMF, are advocating for a closer examination of the potential financial system risks posed by insurers influenced by private equity entities.

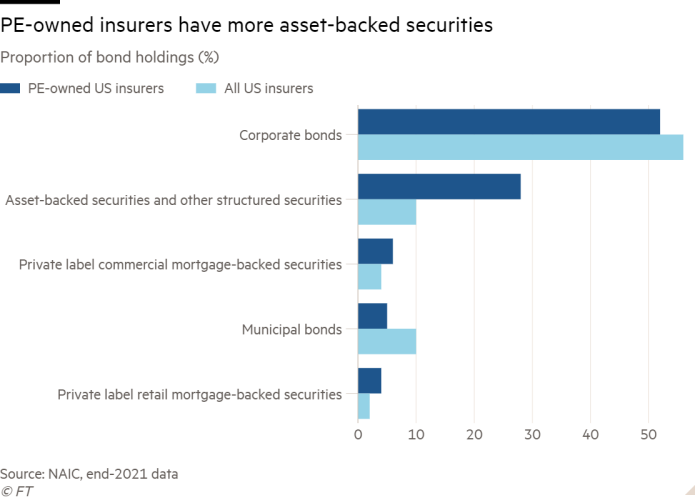

The shift in ownership dynamics has raised concerns about conflicting interests, elevated risk exposure, and governance issues, necessitating enhanced supervision. The International Association of Insurance Supervisors has underscored the complexity and opacity of ownership structures involving private equity, which could impede risk identification and monitoring.

Private capital groups defend their ownership as a means of fortifying life insurers and injecting essential capital into the industry. While some express confidence in managing liquidity risks through stringent asset-liability practices, others caution against the sector’s evolving investment strategies potentially mirroring past financial crises.

Amidst ongoing regulatory discussions and market scrutiny, the insurance industry faces a pivotal juncture where the balance between growth, stability, and risk management will shape its trajectory in the years to come.

\ Get the latest news /